↖

Go to Main

Trackup

Trackup

Making budgeting usable in real life

Mobile

B2C

Overview

TrackyUp is a mobile-first budgeting experience designed for real-world usage — where attention is low, tracking is inconsistent, and financial decisions happen in the moment.

Instead of adding more features, the focus was on reducing the effort required to build a sustainable habit.

Problem

Budgeting doesn’t fail because people lack intent. It fails because the tools don’t align with real behavior.

Most budgeting apps:

1. Require effort at the wrong time

2. Interrupt real-life moments

3. Feel rigid or overwhelming

4. React only after overspending

As a result, users start with intent — but rarely sustain the habit.

Context

Most tools assume users will:

1. Sit down

2. Plan finances

3. Track consistently

But real usage is reactive.

People open budgeting apps when something goes wrong:

1. A failed transaction

2. A low balance alert

3. A moment of financial anxiety

This creates a gap between how tools are designed and how they are actually used.

My role

As a Freelancer, I collaborated closely with the client and engineers to define the user experience for tracking flow. I led the end-to-end design process, from discovery to final UI bringing in user-centered thinking, wireframes and high-fidelity prototypes. My role was to ensure that design aligned with business goals while maintaining a seamless and intuitive experience for users.

Research

To understand this gap, I combined personal experience with lightweight validation:

1. Survey with 40+ participants

2.LinkedIn polls

3. Competitive analysis of 6+ apps

The goal was to reduce friction at the moment of action and make budgeting a habit users could realistically sustain.

Ideation

The design philosophy revolved around effortless simplicity. Every interaction was crafted to minimize friction and guide users naturally through the payment process.

Friction-free expense tracking

Problem

Existing apps required too many steps to log a simple expense.

Decision

Reduce expense logging to a single-step action.

Why

In real-world usage, users prioritize speed over structure.

Solution

1. Open app → Add amount → Done.

2. Optional categorization later.

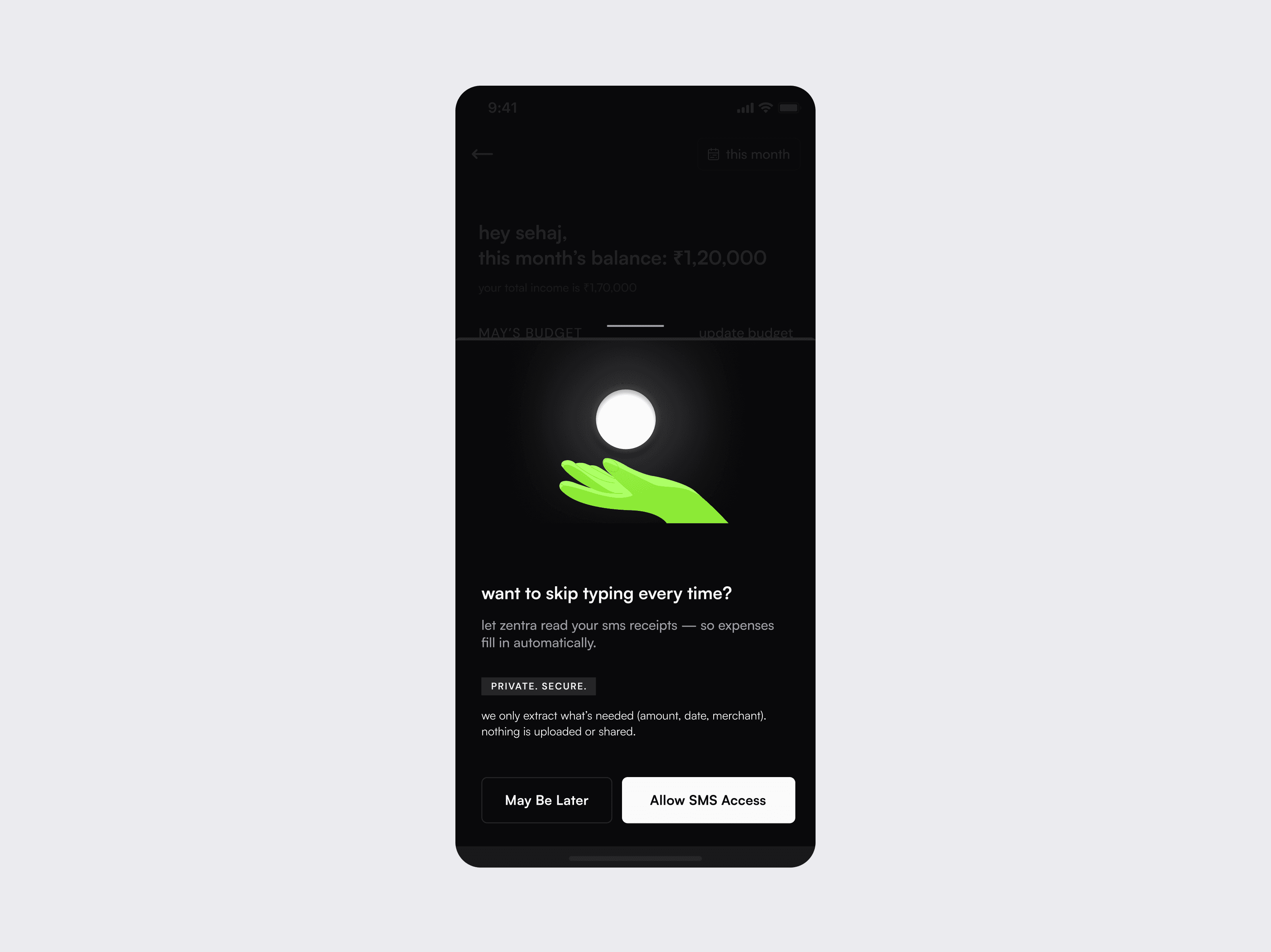

3. Smart SMS parsing (with permission).

4. Local processing (privacy-first).

Remove heavy onboarding

Problem

Users dropped off before experiencing value due to upfront setup.

Decision

Replace onboarding with progressive disclosure.

Why

Reducing cognitive load early increases adoption and trust.

Solution

1. No mandatory setup at entry.

2. Features introduced gradually.

3. Contextual prompts instead of upfront forms.

Make financial status instantly clear

Problem

Users struggled to interpret dashboards and numbers quickly.

Decision

Replace data-heavy views with state-based grouping.

Why

Users need quick understanding, not analysis.

Solution

1. Categories grouped as:

a. Under budget.

b. Near limit.

c. Over budget.

2. Visual color indicators (green / yellow / red).

3. Key insights surfaced upfront.

Prevent overspending before it happens

Problem

Most apps notify users only after overspending.

Decision

Introduce proactive, buffer-based alerts.

Why

Users need time to adjust behavior before crossing limits.

Solution

1. Custom thresholds (e.g., 80%).

2. Alerts before limits are reached.

3. Neutral, non-judgmental tone.

Balance automation with user trust

Problem

Automated tools either created noise or required intrusive access.

Decision

Enable permission-based, local automation.

Why

Users want convenience without losing control or privacy.

Solution

1. SMS parsing with explicit consent.

2. Local data processing (no server dependency).

3. User retains full control over entries.

Reduce friction for offline expenses

Problem

Manual entry for offline purchases increased effort.

Decision

Introduce bill scanning with OCR.

Why

Maintains low effort across both online and offline transactions.

Solution

1. Scan or upload receipt.

2. Auto-extract amount, merchant, date.

3. Editable fields for accuracy.

Testing

Tested with 6 users, focusing on speed and first-time experience.

Key observations:

- Faster task completion in quick-add flow

- High adoption of bill scanning

- Positive response to proactive alerts

Closing notes

Designing TrackyUp reinforced a simple idea — the most effective products don’t add more features, they reduce the effort required to use them.

This principle continues to shape how I approach product design.

Read Next

Earn markets

Market Deposit

$97689.32

Net Apr

3.476%

Market

Price

Wallet Balance

Liquidity

Net Apr

USDC

60.81K

23.879

9.780%

$1.0000

Supply

USDT

43.39K

19.989

13.850%

$1.0000

20.3%

Supply

37.118

0.280%

51

wETH

$2.751k

12.8%

Supply

$97.77K

0.0664

1.570%

0.000

wBTC

Supply

My Positions

Total Positons

$567.876

Net Apr

3.476%

Market

Value

Apr

3.347%

21.487

Withdraw

Add

rUSDC

21.487

3.347%

rUSDT

Withdraw

Add

0.9

3.347%

rETH

Withdraw

Add

Supply

Supply

1 rUSDC

1.20

USDC

rUSDC minted (est)

1234.5

USDC

Apr

0.15%

Supply apr

5.73%

HSTK rewards

5.73%

Fees

23.9%

Network fees

0.0003

ETH

Dapp fees

0.15%

Third party Dapp fees

5.73%

Amount

00.000

USDC

MAX

Wallet balance:

100.31 USDC

50%

0%

100%

75%

50%

25%

Select market

USDC

Hashstack

Earn

Borrow

03xf........768cvd

Hashstack

Simplifying a DeFi lending protocol for real-world users

Web3

SaaS

Web & Mobile

B2C

© 2025 Sehaj Sharma